The International Monetary Fund’s (IMF) vision for the future appears to be on par with that of the Chinese Communist Party (CCP). Soon, your internet browsing history may play a role in the amount of money you’re allowed to borrow.

Researchers at the IMF have published a blog article on their website, suggesting Fintech (financial technology) as the future of America’s credit system.

The article reads: “Recent IMF and ECB staff research distinguishes two areas of financial innovation. One is information: new tools to collect and analyse data on customers, for example for determining creditworthiness. Another is communication: new approaches to customer relationships and the distribution of financial products. We argue that each dimension contains some transformative components”

The article continues, “The most transformative information innovation is the increase in use of new types of data coming from the digital footprint of customers’ various online activities—mainly for credit-worthiness analysis.”

“Credit scoring using so-called hard information (income, employment time, assets and debts) is nothing new. Typically, the more data is available, the more accurate is the assessment. But this method has two problems. First, hard information tends to be “procyclical”: it boosts credit expansion in good times but exacerbates contraction during downturns.” the IMF blog article states.

“The second and most complex problem is that certain kinds of people, like new entrepreneurs, innovators and many informal workers might not have enough hard data available. Even a well-paid expatriate moving to the United States can be caught in the conundrum of not getting a credit card for lack of credit record, and not having a credit record for lack of credit cards.”

“Fintech resolves the dilemma by tapping various nonfinancial data: the type of browser and hardware used to access the internet, the history of online searches and purchases. Recent research documents that, once powered by artificial intelligence and machine learning, these alternative data sources are often superior than traditional credit assessment methods, and can advance financial inclusion, by, for example, enabling more credit to informal workers and households and firms in rural areas.” states the IMF article.

“Governments should follow and carefully support the technological transition in finance. It is important to adjust policies accordingly and stay ahead of the curve.” the article concludes.

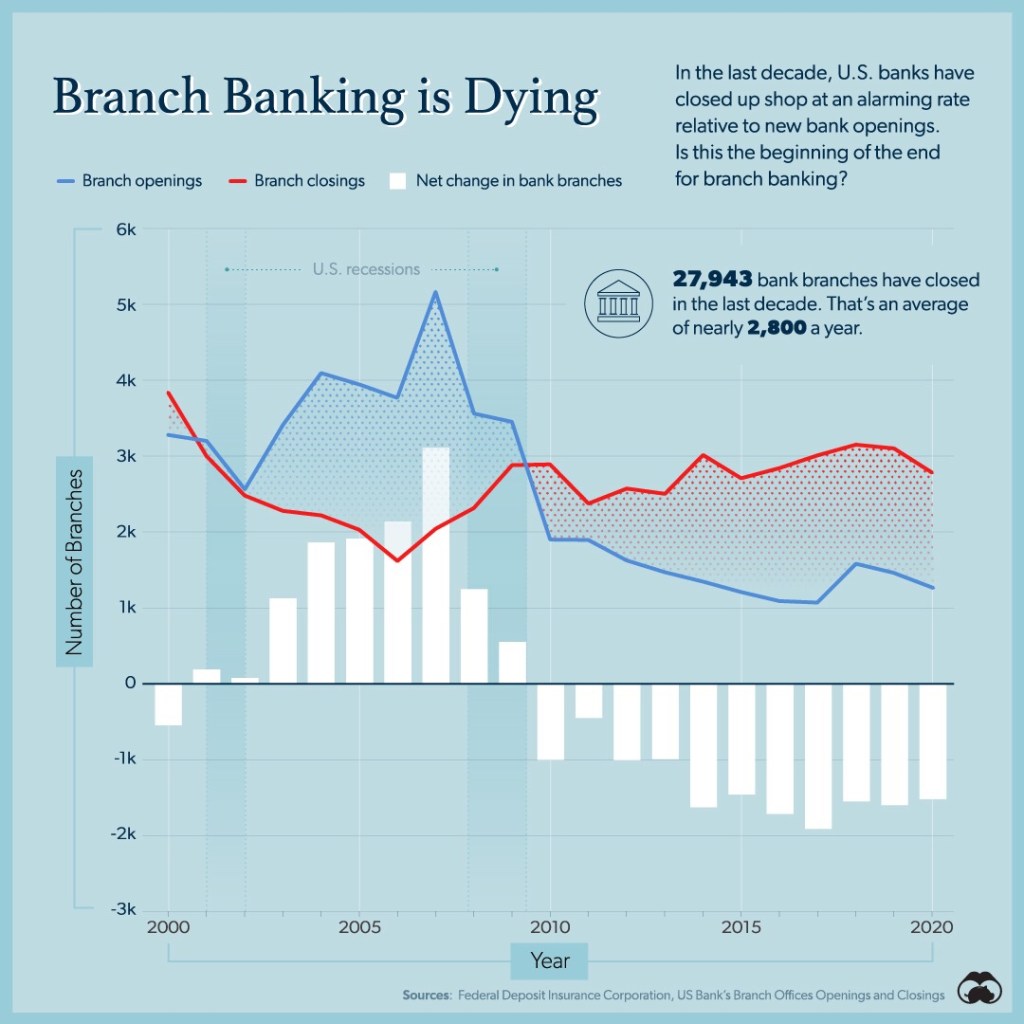

The Fall of Branch Banking

Branch banking is dying. In the last decade 27,943 bank branches have closed. That is an average loss of 2,800 banks per year. In America, 29% of banking is done via mobile, where as in China 81% of banking is done via mobile.

“Historically, banks were local businesses that liaised with customers in a physical branch location. The associated spatial capture allowed banks to exert considerable market power. While early technological innovations, such as the ATM and telephone banking, increased convenience for customers and reduced costs for banks, banking largely remained a brick- and-mortar business” – IMF

The Rise of Fintech

“Bigtech firms have the informational capacity to compete, and possibly even outperform banks in financial service provision. This is corroborated by Frost et al. (2019), who show that the internal ratings of MercadoLibre, an online marketplace in Latin America, predict default risk better than credit scores.” – IMF

IMF Blog

The International Monetary Fund released a blog article depicting the data, and providing a suggestion to these problems.

A 2020 publication by the IMF reads, “The use of non-financial data will have large effects on the provision of financial services. Traditionally, banks rely on the analysis of customer financial information from payment flows and accounting records. The rise of the internet permits the use of new types of non- financial customer data, such as browsing histories and online shopping behavior of individuals, or customer ratings for online vendors.”

“These advantages come at the risk that hard information may become monopolized. Bigtech firms and other platforms may have privileged access to customer data, or their scale provides them with relative advantages in collecting and processing information.”

Previous 2019 Study

Previously, a 66-page study was created in 2019 analyzing “credit scores” using “digital footprints”.

Conclusion

This implementation will create a social credit score directly similar to the Chinese Communist Party regime. With vaccine passports and mandated coronavirus concoctions already causing a division between American citizens, will this be the next phase of social control our U.S. population will face?